One waterway. One conflict. Half of global plastic production offline in a matter of days.

If you buy, make, or sell anything in packaging, this affects you — and it's not going away anytime soon.

What happened

On March 12th, crude oil hit $126 per barrel. Polymer prices surged 41% to 80% in the weeks that followed, resulting in ~50% of global polyethylene capacity now offline or severely constrained.

It all traces back to the Strait of Hormuz — a narrow passage in the Persian Gulf that most people in the packaging industry have never had to think about. Until now.

This waterway handles 15 to 20 million barrels of oil per day. That's 20 to 34% of global oil trade. It also carries most Middle Eastern polyethylene exports, plus 80% of the naphtha Asian manufacturers rely on to make plastic.

Close it down, and the entire global plastics supply chain seizes up.

It's worse than the oil price suggests

Here's what makes this crisis different from previous shocks: polymer prices are still climbing even as crude oil comes back down.

For the first time, polymer prices have decoupled from oil. They used to move together almost perfectly. Now they don't.

India's prices are up 60% since the crisis started. Europe's LLDPE has risen around 44% month over month. Southeast Asia is up around ~50%. The CEO of Dow Chemical was blunt about it: "this isn't resolving for the rest of the year, even if the conflict ended tomorrow".

Why? Because this is a double hit — and each side of it is serious.

On the production side, Middle Eastern exporters can't get their material to market. Qatar halted all polymer production from March 2nd. Over 40 energy assets in the region have been damaged or disrupted. 31 force majeure declarations have been issued across the petrochemical industry.

On the feedstock side, Asian producers — typically among the cheapest in the world — can't access the naphtha they need. Their supply is cut off. They can't fulfil orders.

A market that was oversupplied just weeks ago has flipped. There simply isn't enough virgin resin to go around.

The insurance problem nobody is talking about

Before this conflict, insuring a $100 million tanker cost around $75,000. It now costs around $5 million.

That's a 4,000% increase in risk premiums. Major insurers have cancelled their war risk cover entirely. And because insurers typically only reassess their rates every six months, those costs won't normalize for at least a year — regardless of when or how the conflict ends.

Every barrel of oil being shipped through this region now carries a $10 risk surcharge, baked in purely because the market is too volatile to price otherwise. Container surcharges of $1,500 to $4,000 per unit are being added on top.

These costs flow downstream, into your packaging and onto your shelves.

What this means for your costs — by material

Plastics are the hardest hit. If your packaging relies on virgin polyethylene (PE) or polypropylene (PP), you're already seeing the impact or you're about to. Supply is constrained globally, prices are elevated, and chemical companies are increasingly aware that this is the new normal for the foreseeable future.

Paper is facing pressure too, but from a different angle. Energy makes up 15 to 20% of paper mill production costs, and energy prices are up. US-based mills are more insulated due to domestic oil production; Asian operations are significantly more exposed. OCC hit $91 per ton in April and is continuing to climb.

Aluminum is at a four-year high — around $3,571 per ton in mid-April. Virgin aluminum is energy-intensive to produce at the best of times. Right now, both energy and raw material costs are elevated, and the supply chain disruption in the Middle East is compounding the problem.

The cycle brands need to break

Here's the uncomfortable truth for procurement and sustainability teams: we've been here before, and the industry has handled it badly every time.

Virgin resin gets expensive. Brands rush towards recycled content. Recyclers try to scale up. Supply can't keep pace with demand. Oil corrects. Virgin gets cheap again. Interest in recycled content evaporates. Recyclers who invested get burned.

That's been the pattern — through the 2008 OPEC crisis, through National Sword, through every previous price shock.

The brands that have relied on virgin material as a default haven't just been making a sustainability trade-off. They've been building supply chain fragility into their operations, one contract at a time.

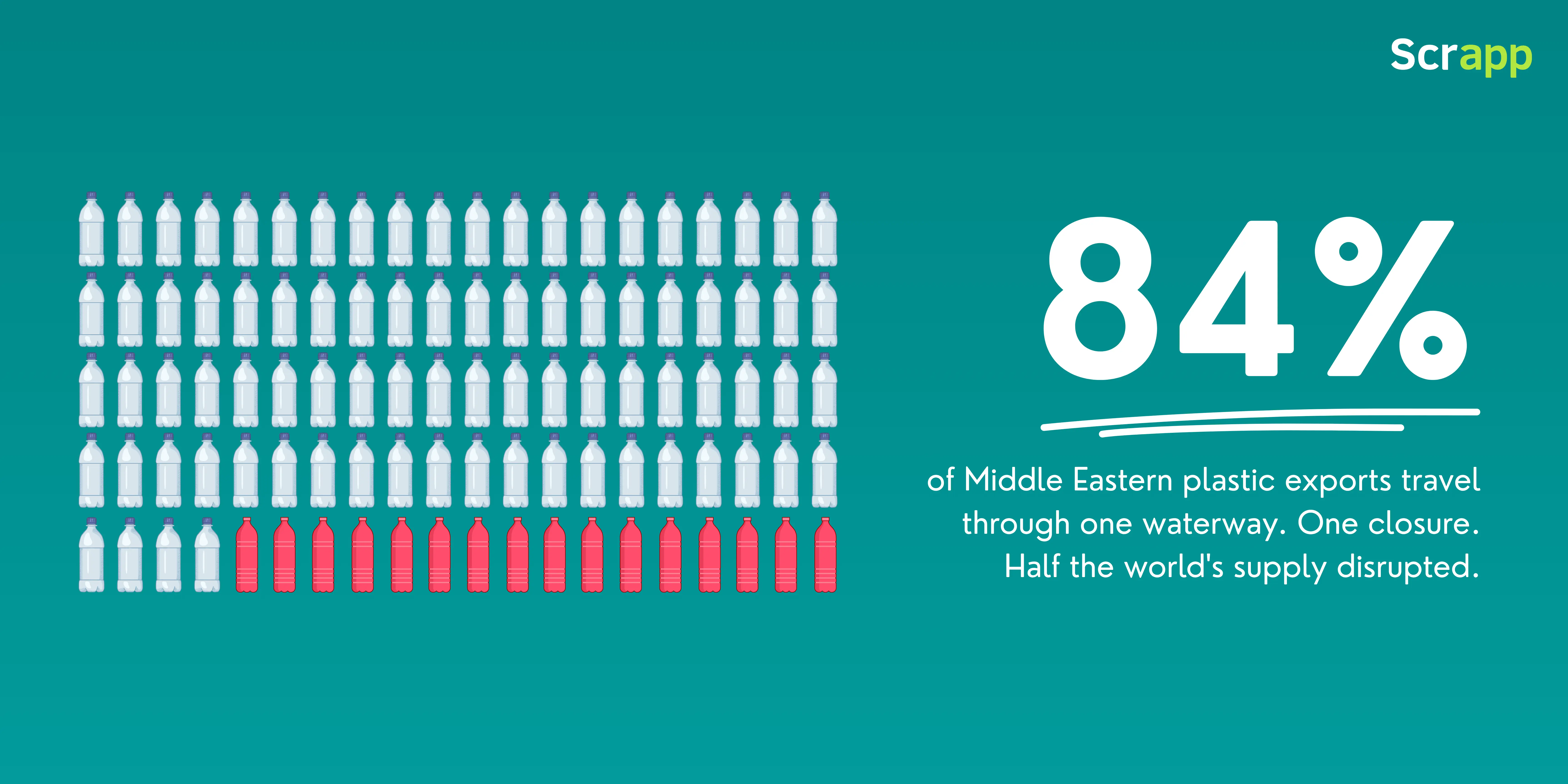

84% of Middle Eastern polyethylene (PE) moves through a single waterway. It took one conflict to take out 50% of global PE capacity in days. That is not a risk that can be managed reactively.

3 things to act on now

1. Map your exposure. If you don't know exactly which of your materials are sourced from Middle Eastern or Asian producers, now is the time to find out. The brands least impacted by this crisis are the ones who already knew where their supply chain was fragile.

2. Treat recycled content as supply chain insurance, not just a compliance exercise. Recycled PET flake is currently around 300 euros per ton cheaper than virgin. Recycled materials are largely sourced and processed domestically. They don't move through the Strait of Hormuz. For the first time, the economics and the risk argument point in the same direction.

3. Don't wait for the crisis to pass before making decisions. The historical pattern is that interest in recycled materials spikes during crises and collapses once virgin resin gets cheap again. But EPR and PPWR compliance targets don't move with commodity markets. If you're going to have to retool for recycled content by 2030 anyway, doing it now — when the price advantage is real — is a better business decision than waiting.

In Conclusion

This isn't a temporary spike to weather. The CEO of Dow Chemical said the rest of the year is already settled. Insurance costs won't normalize for at least 12 months. The infrastructure damage in the Middle East takes time to repair or replace.

Your packaging costs are going up. The question is how much control you want to have over what happens next.

Scrapp is a waste data tracking platform helping businesses, brands, and communities reduce their waste. We make zero-waste simple by giving organizations the digital tools they need to track waste, prove compliance, and save money.

Want to get a clearer picture of your waste data and packaging exposure? Get in touch.